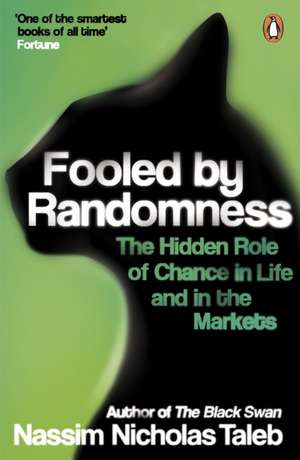

Fooled by Randomness: Bestsellers Taleb

Autor Nassim Nicholas Taleben Limba Engleză Paperback – 3 mai 2007

Remarcăm, înainte de orice, că Fooled by Randomness nu este un tratat teoretic, ci un set de instrumente intelectuale concepute pentru a demonta iluzia cauzalității în medii dominate de incertitudine. Nassim Nicholas Taleb ne oferă cadre de analiză riguroase pentru a distinge între performanța reală și „supraviețuirea celui mai puțin apt”, un fenomen în care indivizi fără competențe reale ajung în poziții de succes exclusiv prin hazard. Notăm cu interes modul în care autorul utilizează profiluri psihologice și șabloane de comportament — precum personajul Nero — pentru a evidenția cum superstițiile moderne ne întunecă judecata în afaceri și investiții. Subliniem că acest volum reprezintă piatra de temelie a seriei Incerto, fiind lucrarea care a stabilit temele fundamentale dezvoltate ulterior de autor. Dacă în The Bed of Procrustes Taleb recurge la aforisme pentru a expune contradicțiile vieții moderne, în Fooled by Randomness el construiește o argumentație solidă împotriva subestimării influenței întâmplării. Complementar volumului The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing, care oferă o metodologie statistică de diferențiere a abilităților, lucrarea lui Taleb acoperă zona psihologică și filosofică a „păcălelii”, explicând de ce suntem programați biologic să vedem modele acolo unde există doar zgomot. Structura narativă este alertă, alternând între experiențele de pe bursa din Wall Street și referințe clasice, de la Solon la Karl Popper. Rezultatul este o disciplinare a gândirii: cititorul învață să aplice un scepticism constructiv în fața „guru-șilor” și a strategiilor care nu pot fi replicate deoarece au fost obținute prin noroc chior.

Preț: 92.27 lei

Carte disponibilă

Livrare economică 17-31 august

Livrare express 31 iulie-06 august pentru 22.71 lei

Specificații

ISBN-10: 0141031484

Pagini: 291

Dimensiuni: 128 x 197 x 25 mm

Greutate: 0.28 kg

Editura: Penguin Books

Colecția Penguin

Seria Bestsellers Taleb

Locul publicării:London, United Kingdom

V-ar putea interesa

-

A Clash of KingsGeorge R. R. MartinPreț: 54.02 lei

A Clash of KingsGeorge R. R. MartinPreț: 54.02 lei -

The Power Of ShapeRon Klinger-28%Preț: 65.08 lei90.68 lei

The Power Of ShapeRon Klinger-28%Preț: 65.08 lei90.68 lei -

The Golden Rules of Competitive AuctionsJulian Pottage-28%Preț: 55.72 lei77.11 lei

The Golden Rules of Competitive AuctionsJulian Pottage-28%Preț: 55.72 lei77.11 lei -

Adventures In Card PlayHugh Kelsey-27%Preț: 86.90 lei119.66 lei

Adventures In Card PlayHugh Kelsey-27%Preț: 86.90 lei119.66 lei -

The Truth about the Drug CompaniesMarcia Angell-30%Preț: 84.99 lei121.88 lei

The Truth about the Drug CompaniesMarcia Angell-30%Preț: 84.99 lei121.88 lei -

Hedge Funds in Emerging MarketsGordon De BrouwerPreț: 299.41 lei

Hedge Funds in Emerging MarketsGordon De BrouwerPreț: 299.41 lei -

DNS and BindCricket Liu-20%Preț: 305.68 lei382.11 lei

DNS and BindCricket Liu-20%Preț: 305.68 lei382.11 lei -

-28%Preț: 65.71 lei91.05 lei

-28%Preț: 65.71 lei91.05 lei -

Bidding in the 21st CenturyAudrey GrantPreț: 136.99 lei

Bidding in the 21st CenturyAudrey GrantPreț: 136.99 lei -

AntifragileNassim Nicholas TalebPreț: 208.87 lei

AntifragileNassim Nicholas TalebPreț: 208.87 lei -

New Frontiers for Strong Forcing OpeningsKenneth RexfordPreț: 85.56 lei

New Frontiers for Strong Forcing OpeningsKenneth RexfordPreț: 85.56 lei -

A Modern Approach to Two-Over-OneKen EichenbaumPreț: 73.10 lei

A Modern Approach to Two-Over-OneKen EichenbaumPreț: 73.10 lei -

The Trouble with Medical JournalsRichard Smith-5%Preț: 380.23 lei400.24 lei

The Trouble with Medical JournalsRichard Smith-5%Preț: 380.23 lei400.24 lei -

Positive Defense at BridgeTerence ReesePreț: 102.61 lei

Positive Defense at BridgeTerence ReesePreț: 102.61 lei -

Cuebidding at Bridge: A Modern ApproachKen RexfordPreț: 110.13 lei

Cuebidding at Bridge: A Modern ApproachKen RexfordPreț: 110.13 lei -

Preț: 216.81 lei

Preț: 216.81 lei -

The Rodwell FilesEric RodwellPreț: 162.17 lei

The Rodwell FilesEric RodwellPreț: 162.17 lei -

Contested AuctionRoy HughesPreț: 151.38 lei

Contested AuctionRoy HughesPreț: 151.38 lei

De ce să citești această carte

Această carte se adresează profesioniștilor din finanțe, antreprenorilor și oricui dorește să navigheze mai lucid într-o lume imprevizibilă. Veți câștiga o imunitate sporită în fața narativelor false despre succes și veți învăța să recunoașteți limitele previziunilor umane. Este un ghid esențial pentru a înțelege că, de multe ori, ceea ce numim strategie este doar o coincidență favorabilă.

Despre autor

Nassim Nicholas Taleb este un eseist libanezo-american, statistician și fost trader de opțiuni, specializat în problemele incertitudinii și probabilității. Este autorul celebrei serii Incerto, o investigație filosofică în cinci volume despre riscul în lumea reală. Recunoscut pentru capacitatea sa de a anticipa crizele financiare, Taleb a fost profesor la universități de prestigiu, inclusiv NYU Tandon School of Engineering. Opera sa, care include titluri precum The Black Swan și Antifragile, pledează pentru construirea unor sisteme reziliente în fața evenimentelor imprevizibile, transformând radical modul în care instituțiile globale percep gestionarea riscului.

Notă biografică

Nassim Nicholas Taleb spent twenty-one years as a risk taker before becoming a researcher in philosophical, mathematical, and (mostly) practical problems with probability. Although he spends most of his time as a flâneur, meditating in cafes across the planet, he is currently Distinguished Professor at New York University's Tandon School of Engineering but self-funds his own research.

His books, Antifragile, The Black Swan, The Bed of Procrustes and Fooled by Randomness (part of a multi-volume collection called Incerto, Latin for uncertainty), have been translated into thirty-seven languages. Taleb has authored more than fifty scholarly papers as backup to Incerto, ranging from international affairs and risk management to statistical physics. He refuses all awards and honours as they debase knowledge by turning it into competitive sports.

Descriere scurtă

Everyone wants to succeed in life. But what causes some of us to be more successful than others? Is it really down to skill and strategy - or something altogether more unpredictable?

This book is the bestselling sensation that will change the way you think about business and the world. It is all about luck: more precisely, how we perceive luck in our personal and professional experiences. Nowhere is this more obvious than in the markets - we hear an entrepreneur has 'vision' or a trader is 'talented', but all too often their performance is down to chance rather than skill. It is only because we fail to understand probability that we continue to believe events are non-random, finding reasons where none exist.

'One of the smartest books of all time' Fortune

'An iconoclastic tour de force ... nothing escapes his Exocets' Evening Standard

'Brilliant' John Kay

'Excellent and thought-provoking ... an entertaining book' Financial Times

'Wall Street's principal dissident' Malcolm Gladwell

Extras

Croesus, King of Lydia, was considered the richest man of his time. To this day Romance languages use the expression “rich as Croesus” to describe a person of excessive wealth. He was said to be visited by Solon, the Greek legislator known for his dignity, reserve, upright morals, humility, frugality, wisdom, intelligence, and courage. Solon did not display the smallest surprise at the wealth and splendor surrounding his host, nor the tiniest admiration for their owner. Croesus was so irked by the manifest lack of impression on the part of this illustrious visitor that he attempted to extract from him some acknowledgment. He asked him if he had known a happier man than him. Solon cited the life of a man who led a noble existence and died while in battle. Prodded for more, he gave similar examples of heroic but terminated lives, until Croesus, irate, asked him point-blank if he was not to be considered the happiest man of all. Solon answered: “The observation of the numerous misfortunes that attend all conditions forbids us to grow insolent upon our present enjoyments, or to admire a man’s happiness that may yet, in course of time, suffer change. For the uncertain future has yet to come, with all variety of future; and him only to whom the divinity has [guaranteed] continued happiness until the end we may call happy.”

The modern equivalent has been no less eloquently voiced by the baseball coach Yogi Berra, who seems to have translated Solon’s outburst from the pure Attic Greek into no less pure Brooklyn English with “it ain’t over until it’s over,” or, in a less dignified manner, with “it ain’t over until the fat lady sings.” In addition, aside from his use of the vernacular, the Yogi Berra quote presents an advantage of being true, while the meeting between Croesus and Solon was one of those historical facts that benefited from the imagination of the chroniclers, as it was chronologically impossible for the two men to have been in the same location.

Part I is concerned with the degree to which a situation may yet, in the course of time, suffer change. For we can be tricked by situations involving mostly the activities of the goddess Fortuna—Jupiter’s firstborn daughter. Solon was wise enough to get the following point; that which came with the help of luck could be taken away by luck (and often rapidly and unexpectedly at that). The flipside, which deserves to be considered as well (in fact it is even more of our concern), is that things that come with little help from luck are more resistant to randomness. Solon also had the intuition of a problem that has obsessed science for the past three centuries. It is called the problem of induction. I call it in this book the black swan or the rare event. Solon even understood another linked problem, which I call the skewness issue; it does not matter how frequently something succeeds if failure is too costly to bear.

Yet the story of Croesus has another twist. Having lost a battle to the redoubtable Persian king Cyrus, he was about to be burned alive when he called Solon’s name and shouted (something like) “Solon, you were right” (again this is legend). Cyrus asked about the nature of such unusual invocations, and he told him about Solon’s warning. This impressed Cyrus so much that he decided to spare Croesus’ life, as he reflected on the possibilities as far as his own fate was concerned. People were thoughtful at that time.

If You’re So Rich, Why Aren’t You So Smart?

An illustration of the effect of randomness on social pecking order and jealousy, through two characters of opposite attitudes. On the concealed rare event. How things in modern life may change rather rapidly, except, perhaps, in dentistry.

Nero Tulip

Hit by Lightning

Nero Tulip became obsessed with trading after witnessing a strange scene one spring day as he was visiting the Chicago Mercantile Exchange. A red convertible Porsche, driven at several times the city speed limit, abruptly stopped in front of the entrance, its tires emitting the sound of pigs being slaughtered. A visibly demented athletic man in his thirties, his face flushed red, emerged and ran up the steps as if he were chased by a tiger. He left the car double-parked, its engine running, provoking an angry fanfare of horns. After a long minute, a bored young man clad in a yellow jacket (yellow was the color reserved for clerks) came down the steps, visibly untroubled by the traffic commotion. He drove the car into the underground parking garage—perfunctorily, as if it were his daily chore.

That day Nero Tulip was hit with what the French call a coup de foudre, a sudden intense (and obsessive) infatuation that strikes like lightning. “This is for me!” he screamed enthusiastically—he could not help comparing the life of a trader to the alternative lives that could present themselves to him. Academia conjured up the image of a silent university office with rude secretaries; business, the image of a quiet office staffed with slow thinkers and semislow thinkers who express themselves in full sentences.

Temporary Sanity

Unlike a coup de foudre, the infatuation triggered by the Chicago scene has not left him more than a decade and a half after the incident. For Nero swears that no other lawful profession in our times could be as devoid of boredom as that of the trader. Furthermore, although he has not yet practiced the profession of high-sea piracy, he is now convinced that even that occupation would present more dull moments than that of the trader.

Nero could best be described as someone who randomly (and abruptly) swings between the deportment and speech manners of a church historian and the verbally abusive intensity of a Chicago pit trader. He can commit hundreds of millions of dollars in a transaction without a blink or a shadow of a second thought, yet agonize between two appetizers on the menu, changing his mind back and forth and wearing out the most patient of waiters.

Nero holds an undergraduate degree in ancient literature and mathematics from Cambridge University. He enrolled in a Ph.D. program in statistics at the University of Chicago but, after completing the prerequisite coursework, as well as the bulk of his doctoral research, he switched to the philosophy department. He called the switch “a moment of temporary sanity,” adding to the consternation of his thesis director, who warned him against philosophers and predicted his return back to the fold. He finished writing his thesis in philosophy. But not the Derrida continental style of incomprehensible philosophy (that is, incomprehensible to anyone outside of their ranks, like myself). It was quite the opposite; his thesis was on the methodology of statistical inference in its application to the social sciences. In fact, his thesis was indistinguishable from a thesis in mathematical statistics—it was just a bit more thoughtful (and twice as long).

It is often said that philosophy cannot feed its man—but that was not the reason Nero left. He left because philosophy cannot entertain its man. At first, it started looking futile; he recalled his statistics thesis director’s warnings. Then, suddenly, it started to look like work. As he became tired of writing papers on some arcane details of his earlier papers, he gave up the academy. The academic debates bored him to tears, particularly when minute points (invisible to the noninitiated) were at stake. Action was what Nero required. The problem, however, was that he selected the academy in the first place in order to kill what he detected was the flatness and tempered submission of employment life.

After witnessing the scene of the trader chased by a tiger, Nero found a trainee spot on the Chicago Mercantile Exchange, the large exchange where traders transact by shouting and gesticulating frenetically. There he worked for a prestigious (but eccentric) local, who trained him in the Chicago style, in return for Nero solving his mathematical equations. The energy in the air proved motivating to Nero. He rapidly graduated to the rank of self-employed trader. Then, when he got tired of standing on his feet in the crowd, and straining his vocal cords, he decided to seek employment “upstairs,” that is, trading from a desk. He moved to the New York area and took a position with an investment house.

Nero specialized in quantitative financial products, in which he had an early moment of glory, became famous and in demand. Many investment houses in New York and London flashed huge guaranteed bonuses at him. Nero spent a couple of years shuttling between the two cities, attending important “meetings” and wearing expensive suits. But soon Nero went into hiding; he rapidly pulled back to anonymity—the Wall Street stardom track did not quite fit his temperament. To stay a “hot trader” requires some organizational ambitions and a power hunger that he feels lucky not to possess. He was only in it for the fun—and his idea of fun does not include administrative and managerial work. He is susceptible to conference room boredom and is incapable of talking to businessmen, particularly the run-of-the-mill variety. Nero is allergic to the vocabulary of business talk, not just on plain aesthetic grounds. Phrases like “game plan,” “bottom line,” “how to get there from here,” “we provide our clients with solutions,” “our mission,” and other hackneyed expressions that dominate meetings lack both the precision and the coloration that he prefers to hear. Whether people populate silence with hollow sentences, or if such meetings present any true merit, he does not know; at any rate he did not want to be part of it. Indeed Nero’s extensive social life includes almost no businesspeople. But unlike me (I can be extremely humiliating when someone rubs me the wrong way with inelegant pompousness), Nero handles himself with gentle aloofness in these circumstances.

So, Nero switched careers to what is called proprietary trading. Traders are set up as independent entities, internal funds with their own allocation of capital. They are left alone to do as they please, provided of course that their results satisfy the executives. The name proprietary comes from the fact that they trade the company’s own capital. At the end of the year they receive between 7% and 12% of the profits generated. The proprietary trader has all the benefits of self-employment, and none of the burdens of running the mundane details of his own business. He can work any hours he likes, travel at a whim, and engage in all manner of personal pursuits. It is paradise for an intellectual like Nero who dislikes manual work and values unscheduled meditation. He has been doing that for the past ten years, in the employment of two different trading firms.

Modus Operandi

A word on Nero’s methods. He is as conservative a trader as one can be in such a business. In the past he has had good years and less than good years—but virtually no truly “bad” years. Over these years he has slowly built for himself a stable nest egg, thanks to an income ranging between $300,000 and (at the peak) $2.5 million. On average, he manages to accumulate $500,000 a year in after-tax money (from an average income of about $1 million); this goes straight into his savings account. In 1993, he had a bad year and was made to feel uncomfortable in his company. Other traders made out much better, so the capital at his disposal was severely reduced, and he was made to feel undesirable at the institution. He then went to get an identical job, down to an identically designed workspace, but in a different firm that was friendlier. In the fall of 1994 the traders who had been competing for the great performance award blew up in unison during the worldwide bond market crash that resulted from the random tightening by the Federal Reserve Bank of the United States. They are all currently out of the market, performing a variety of tasks. This business has a high mortality rate.

Why isn’t Nero more affluent? Because of his trading style—or perhaps his personality. His risk aversion is extreme. Nero’s objective is not to maximize his profits, so much as it is to avoid having this entertaining machine called trading taken away from him. Blowing up would mean returning to the tedium of the university or the nontrading life. Every time his risks increase, he conjures up the image of the quiet hallway at the university, the long mornings at his desk spent in revising a paper, kept awake by bad coffee. No, he does not want to have to face the solemn university library where he was bored to tears. “I am shooting for longevity,” he is wont to say.

Nero has seen many traders blow up, and does not want to get into that situation. Blow up in the lingo has a precise meaning; it does not just mean to lose money; it means to lose more money than one ever expected, to the point of being thrown out of the business (the equivalent of a doctor losing his license to practice or a lawyer being disbarred). Nero rapidly exits trades after a predetermined loss. He never sells “naked options” (a strategy that would leave him exposed to large possible losses). He never puts himself in a situation where he can lose more than, say, $1 million—regardless of the probability of such an event. That amount has always been variable; it depends on his accumulated profits for the year. This risk aversion prevented him from making as much money as the other traders on Wall Street who are often called “Masters of the Universe.” The firms he has worked for generally allocate more money to traders with a different style from Nero, like John, whom we will encounter soon.

Nero’s temperament is such that he does not mind losing small change. “I love taking small losses,” he says. “I just need my winners to be large.” In no circumstances does he want to be exposed to those rare events, like panics and sudden crashes, that wipe a trader out in a flash. To the contrary, he wants to benefit from them. When people ask him why he does not hold on to losers, he invariably answers that he was trained by “the most chicken of them all,” the Chicago trader Stevo who taught him the business. This is not true; the real reason is his training in probability and his innate skepticism.

From the Trade Paperback edition.

Recenzii

–Malcolm Gladwell, The New Yorker

“Fascinating . . . Taleb will grab you.”

–Peter L. Bernstein, author of Against the Gods: The Remarkable Story of Risk

“Recalls the best of scientist/essayists like Richard Dawkins . . . and Stephen Jay Gould.”

–Michael Schrage, author of Serious Play

“We need a book like this . . . fun to read, refreshingly independent-minded.”

–Robert J. Shiller, author of Irrational Exuberance

From the Trade Paperback edition.